By Al LewisDow Jones Newswires

Posted: 01/25/2009 12:30:00 AM MST

People with no conscience can do well in business — at least until their schemes unravel.

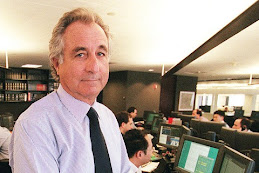

Barry Minkow was one of those people.

"We could walk into a meeting . . . and I could tell a community of Wall Street investors that my company was profitable when I knew it was not — and not blink," he said. "I was a thief and a liar and a crook."

Today, he's different.

"Today, if my wife asked me if I emptied the trash, and I forgot and I say, 'Yes, I did,' I'll run and empty the trash and then feel guilty, and confess that I lied."

He still lies. But now it bothers him.

"Just because I'm not committing securities fraud or perpetrating a Ponzi scheme does not mean that my life is not in dire need of constant improvement," he said.

Minkow now claims to have a conscience, a still-small voice that empathizes, chooses right over wrong, and discerns truth from delusion and deception.

I find it improbable that a renegade businessman can grow a conscience like a salamander grows a lost appendage. But some things about Minkow are improbable.

At age 16, he started a carpet-cleaning outfit called ZZZZ Best Co. in his parents' garage in Inglewood, Calif.

Despite his youth and the low profit margins that such companies are known to generate, Minkow was able to take ZZZZ Best through an initial public stock offering in just a few years.

He claimed a net worth of $90 million, drove a red Ferrari with a "ZZZZ BEST" license plate and appeared on Oprah's show as a Wall Street whiz kid.

As it turned out, though, Minkow booked as revenue the money he had borrowed from the mob, so he could borrow millions more from banks and investors. He forged thousands of documents and leased buildings that he staged as work sites when auditors wanted to check his work.

By age 23, he had been convicted of 57 counts of fraud involving securities, credit cards and the U.S. mail. A memorandum prepared by prosecutors for his 1989 sentencing described him as remorseless.

"You're dangerous because you have this gift of gab, this ability to communicate," U.S. District Judge Dikran Tevrizian told Minkow. "You don't have a conscience."

Minkow told me he didn't have a conscience because he "didn't know the Lord." A Jew, he found Jesus in prison.

After nearly eight years behind bars, he went on to Jerry Falwell's Liberty University, where he earned a master's degree in divinity. He then became pastor of Community Bible Church in San Diego.

In 12 years, he said, his flock has grown from 135 to more than 1,500. "The whole theme of the Bible," said Minkow, now 42, "is that people can change."

In 2001, he started the Fraud Discovery Institute, where he profits by ratting out white-collar miscreants. Sometimes he shorts the stocks of companies he targets. Other times, people hire him for a fee.

This business model may seem ethically challenged to some, but news reports over the years credit him with uncovering about $1.8 billion worth of fraud, many of it in multimillion-dollar Ponzi schemes. He has even received applause from the FBI.

Several executives of publicly traded companies have had to resign after Minkow uncovered fabrications on their resumes, including MGM Mirage's former chief executive, J. Terrence Lanni, who stepped down in November.

"He has done some good things," Tevrizian told CBS's "60 Minutes" in 2005. "He's uncovered several hundreds of millions of dollars' worth of frauds. And I give him credit for that."

Now, Minkow is gunning for Lennar Corp.

On Jan. 9, Minkow started a website, lenn-ron.com, and he has made a YouTube video likening Lennar to Enron and alleged Ponzi-schemer Bernard Madoff.

Immediately after Minkow claimed that Lennar was "a financial crime in progress," Lennar's stock plunged as much as 28 percent. Lennar responded by denying Minkow's claims and filing a lawsuit accusing him of defamation and extortion.

A California developer named Nicolas Marsch III, who has sued Lennar over his partnerships with the homebuilder, is reportedly paying Minkow as much as $100,000.

Lennar said in its lawsuit that Marsch "threatened to air (Lennar's) dirty little secrets if Lennar did not make an immediate payment of $39 million."

Minkow said it's not true, and he claims Lennar's lawsuit will only lead more people to suspect his claims are true.

"Why else would anybody care about what Barry Minkow has to say?" he said.

So far, Lennar stock has yet to recover.

On Wednesday, a San Diego court rejected Lennar's motion for a restraining order and injunction against Minkow's disparaging website.

Whether Minkow has grown a conscience is a matter of faith. But for Lennar, one thing is certain: He's still in business.

Sunday, January 25, 2009

Thursday, January 22, 2009

Obama Inauguration: Slide on Wall Street. Where have all the Creditors Gone?...

"When Will We Ever Learn?" By Michel Chossudovsky | |

dotconnectoruk.blogspot.com January 20, 2009 | |

Across the land, an atmosphere of hope and optimism prevails. The Bush regime has gone. A new president is in the White House. While America had its eyes riveted on the live TV broadcast of Barack Obama's presidential inauguration, financial markets were sliding. Immediately following the inauguration, the Dow Jones plummeted, largely affecting the share prices of major financial institutions. The quoted stock values of major Wall Street banks plummeted. Citigroup fell by 20 percent, Bank of America by 29 percent and JP Morgan Chase by 20 percent. The Royal Bank of Scotland fell by 69 percent in New York trading. Source: Yahoo So why now? The inauguration of a president Obama was expected to provide confidence to financial markets. Exactly the opposite occurred. There was nothing spontaneous and accidental in this collapse of the stock values of amjor financial institutions. Obama's speech outside the Capitol, had been drafted well in advance. Its contents was carefully prepared. President Obama made explicit reference to the global economy's woes, while emphasizing that: "without a watchful eye, the market can spin out of control."

There were "high expectations" on Wall Street. Many Wall Street brokers, who were not privy to the contents of Obama's speech, were "betting" President Obama's statements would help stabilize financial markets. Those who drafted Obama's speech were fully aware of its possible financial repercussions.

Coincidentally, the chairman of the Securities and Exchange Commission, Christopher Cox, appointed by Bush in 2005, resigned on the very same day of the presidential inauguration, leading to vacuum in the adoption of crucial financial regulatory decisions. His successor, Mary Shapiro, will only take office following lengthy Senate confirmation hearings. Those who had advanced knowledge and/or inside information regarding the text of Obama's speech and who had the ability to "move the market" at the right time and the right place, stood to gain in the conduct of major speculative transactions on stock markets and currency exchanges. Were these speculative transactions planned in advance of January 20th? (See Video) Was there a concerted and deliberate effort to "short the market" on the very same day as the presidential inauguration? On currency markets, the movement was in reverse, the US dollar was rising, the Euro, the British Pound and the Canadian dollar were plummeting. Canada's Central Bank Governor chose the date of the presidential inauguration to announce a cut in the interest rate in an apparent "bid to stimulate the economy and boost lending to consumers and businesses". The impact: the Canadian dollar declined dramatically in relation to Greenback. Were have All the Creditors Gone? The largest financial institutions are said to be in troubled waters, indebted to unnamed creditors. Since the onslaught of the financial meltdown, the identity of the creditors remains a mystery. Over the years, the financial establishment has set up private hedge funds invariably registered in the name of wealthy individuals. Large amounts of wealth have been transferred from the large financial institutions to these privately owned hedge funds, which largely escape government regulation. Why are the banks indebted? To whom? Are they the victims or the recipients? Are they the debtors or the creditors? America's largest banks have, over the years, sifted off part of their surplus profits to various proxy financial outfits, hedge funds, accounts registered in tropical offshore banking havens, etc. While these billion dollar transfers are conducted electronically from one financial entity to another, the identity of the creditors is never mentioned. Who is collecting these multibillion debts which are in large part the consequence of financial manipulation? The collapse in bank stock market values was in all likelihood known in advance. The banks had already moved their loot to a safe financial haven. The banks are in troubled water after having received hundred of billions of dollars of bailout money. Where is the bailout money going? Who is cashing in on the multibillion dollar government bailout money? This process is contributing to an unprecedented concentration of private wealth. The financial press acknowledges the existence of billions of dollars of "inter bank debt". But not a word is mentioned about the creditors. For every debtor, there is a creditor. Is this not money which the financial elites owe to themselves? Whoever holds these trillions will eventually pick up the pieces. They will transform their enormous paper wealth into the acquisition of real assets. Waking up the Day After And the day after the hopes and promises of the presidential inauguration, Middle Class Americans who had invested in "safe" bank shares, will come to realize that part of their lifelong savings have once again been confiscated. | |

Wednesday, January 21, 2009

SEC charges missing money manager Nadel with fraud

By MARCY GORDON, AP Business Writer Marcy Gordon,

Ap Business Writer 1 hr 27 mins ago

WASHINGTON – Federal regulators on Wednesday charged a missing hedge fund manager with fraud, saying he misled investors and overstated the value of investments in the six funds by about $300 million.

The Securities and Exchange Commission won a court order freezing the assets of Arthur G. Nadel, of Sarasota, Fla., and other defendants in the case.

Nadel owed investors a $50 million payout, told his wife in a note he felt guilty and threatened to kill himself, according to the Sarasota County Sheriff's Office. The authorities believe that Nadel, 76, planned his Jan. 14 disappearance.

In a lawsuit filed in federal court in Tampa, the SEC said Nadel recently transferred at least $1.25 million from two of the funds to secret bank accounts that he controlled.

Two investment companies co-owned by Nadel, Scoop Capital and Scoop Management, agreed in a settlement with the SEC to injunctions and an asset freeze. They neither admitted nor denied wrongdoing.

According to Scoop Management's internal accountant, there are between 500 and 600 investors nationwide. Last week, many were told that the funds were empty. Sarasota police have been fielding inquiries from around the country and as far away as France.

Robert Wilkes, a 76-year-old retiree in Vero Beach, Fla., who worked in commercial banking, said the SEC's charges against Nadel didn't surprise him.

"He should be charged with fraud," Wilkes told The Associated Press. He wouldn't disclose how much he'd invested with Nadel, but said, "We're going to have to completely revamp our style of living. We're going to have to cut back."

The SEC also is seeking unspecified restitution plus interest from several so-called relief defendants: investment advisers Valhalla Management and Viking Management, and hedge funds Scoop Real Estate, Valhalla Investment Partners, Victory IRA Fund, Victory Fund, Viking IRA Fund and Viking Fund.

Those defendants consented to an asset freeze, also without admitting or denying the allegations. Nadel provided false and misleading information to those companies to be distributed to investors through account statements and other materials, according to the SEC suit.

The agency said Nadel's funds appeared to have assets totaling less than $1 million — while he claimed in sales materials for three of the funds that they had about $342 million in assets as of Nov. 30. The materials also boasted of monthly returns of 11 to 12 percent for several of the funds last year, when they actually had negative results.

An investor in one fund received an account statement for November indicating that her investment was worth almost $420,000. In reality, the entire fund had less than $100,000, according to the SEC.

"Investors should be able to rely on the truthfulness of an account statement and offering materials," David Nelson, director of the SEC's regional office in Miami, said in a statement. "Mr. Nadel's alleged actions deceived investors, and we are seeking to hold him accountable for that misconduct."

Wilkes already has his Florida home on the market and now plans to put his second home in Vermont up for sale.

"It's just been a very traumatic event for us," he said. "Like a bad dream that when you wake up, you find it's not a dream. It's a nightmare."

__

Ap Business Writer 1 hr 27 mins ago

WASHINGTON – Federal regulators on Wednesday charged a missing hedge fund manager with fraud, saying he misled investors and overstated the value of investments in the six funds by about $300 million.

The Securities and Exchange Commission won a court order freezing the assets of Arthur G. Nadel, of Sarasota, Fla., and other defendants in the case.

Nadel owed investors a $50 million payout, told his wife in a note he felt guilty and threatened to kill himself, according to the Sarasota County Sheriff's Office. The authorities believe that Nadel, 76, planned his Jan. 14 disappearance.

In a lawsuit filed in federal court in Tampa, the SEC said Nadel recently transferred at least $1.25 million from two of the funds to secret bank accounts that he controlled.

Two investment companies co-owned by Nadel, Scoop Capital and Scoop Management, agreed in a settlement with the SEC to injunctions and an asset freeze. They neither admitted nor denied wrongdoing.

According to Scoop Management's internal accountant, there are between 500 and 600 investors nationwide. Last week, many were told that the funds were empty. Sarasota police have been fielding inquiries from around the country and as far away as France.

Robert Wilkes, a 76-year-old retiree in Vero Beach, Fla., who worked in commercial banking, said the SEC's charges against Nadel didn't surprise him.

"He should be charged with fraud," Wilkes told The Associated Press. He wouldn't disclose how much he'd invested with Nadel, but said, "We're going to have to completely revamp our style of living. We're going to have to cut back."

The SEC also is seeking unspecified restitution plus interest from several so-called relief defendants: investment advisers Valhalla Management and Viking Management, and hedge funds Scoop Real Estate, Valhalla Investment Partners, Victory IRA Fund, Victory Fund, Viking IRA Fund and Viking Fund.

Those defendants consented to an asset freeze, also without admitting or denying the allegations. Nadel provided false and misleading information to those companies to be distributed to investors through account statements and other materials, according to the SEC suit.

The agency said Nadel's funds appeared to have assets totaling less than $1 million — while he claimed in sales materials for three of the funds that they had about $342 million in assets as of Nov. 30. The materials also boasted of monthly returns of 11 to 12 percent for several of the funds last year, when they actually had negative results.

An investor in one fund received an account statement for November indicating that her investment was worth almost $420,000. In reality, the entire fund had less than $100,000, according to the SEC.

"Investors should be able to rely on the truthfulness of an account statement and offering materials," David Nelson, director of the SEC's regional office in Miami, said in a statement. "Mr. Nadel's alleged actions deceived investors, and we are seeking to hold him accountable for that misconduct."

Wilkes already has his Florida home on the market and now plans to put his second home in Vermont up for sale.

"It's just been a very traumatic event for us," he said. "Like a bad dream that when you wake up, you find it's not a dream. It's a nightmare."

__

Monday, January 19, 2009

Wall Street Woes Drive Oppenheimer Trust Co. To Become A Bank

Wall Street Woes Drive Oppenheimer Trust Co. To Become A Bank

www.njbiz.com

1/19/2009In the wake of a $56 million fraud investigation against its parent, a Florham Park financial services company is moving forward with its bid to become a bank and tap into a federal bailout program.

Oppenheimer Trust Co.’s application to become a bank and change its name to the Oppenheimer Bank and Trust Co. has been accepted by the New Jersey Department of Banking and Insurance, according to an announcement by the New Jersey Bankers Association.

Oppenheimer Trust also wants to sell a chunk of its stock to the federal government under the Troubled Assets Relief Program.

Oppenheimer Trust currently offers investment and other financial services to high-net-worth individuals and families, and not-for-profit and other organizations, according to the company Web site.

In November, following the meltdown of the volatile auction rate securities, or ARS, debt market, the Massachusetts Securities Division filed a fraud complaint against Oppenheimer’s New York parent, Oppenheimer & Co. Inc., and some top executives. Oppenheimer & Co. steered clients to risky ARS, resulting in losses of $56 million, even as the executives unloaded their own holdings, alleged the Massachusetts Securities Division.

Oppenheimer denied the charges, but said it was “reviewing the availability of the TARP program, and other programs recently announced by the federal government, to provide a solution to this serious issue for its clients.”

The New York parent also said that prior to the filing of the Massachusetts complaint, Oppenheimer Trust was preparing an application to the Federal Deposit Insurance Corp. for deposit insurance, and had filed an application to participate in the TARP stock purchase program.

www.njbiz.com

1/19/2009In the wake of a $56 million fraud investigation against its parent, a Florham Park financial services company is moving forward with its bid to become a bank and tap into a federal bailout program.

Oppenheimer Trust Co.’s application to become a bank and change its name to the Oppenheimer Bank and Trust Co. has been accepted by the New Jersey Department of Banking and Insurance, according to an announcement by the New Jersey Bankers Association.

Oppenheimer Trust also wants to sell a chunk of its stock to the federal government under the Troubled Assets Relief Program.

Oppenheimer Trust currently offers investment and other financial services to high-net-worth individuals and families, and not-for-profit and other organizations, according to the company Web site.

In November, following the meltdown of the volatile auction rate securities, or ARS, debt market, the Massachusetts Securities Division filed a fraud complaint against Oppenheimer’s New York parent, Oppenheimer & Co. Inc., and some top executives. Oppenheimer & Co. steered clients to risky ARS, resulting in losses of $56 million, even as the executives unloaded their own holdings, alleged the Massachusetts Securities Division.

Oppenheimer denied the charges, but said it was “reviewing the availability of the TARP program, and other programs recently announced by the federal government, to provide a solution to this serious issue for its clients.”

The New York parent also said that prior to the filing of the Massachusetts complaint, Oppenheimer Trust was preparing an application to the Federal Deposit Insurance Corp. for deposit insurance, and had filed an application to participate in the TARP stock purchase program.

Wall Street's Taxpayer Funded Bail-Out Scam Will Help PAY for Obama Inauguration...

Submitted by SadInAmerica on 2009,

January 18 - 9:19pm.

President-elect Barack Obama has spoken a lot about setting a new standard for ethics and transparency, and he issued an edict that his inaugural committee would bar contributions from corporations, political action committees, lobbyists, labor unions and foreigners.

But as always seems to happen, big financial interests find a way to weigh in with a pile of cash.

The watchdog group Public Citizen says nearly 80 percent of the $35.3 million raised by the Presidential Inaugural Committee to date has come from 211 wealthy donors, including a number from Wall Street firms benefiting from the mushrooming federal bailout.

Louis Sussman, vice chairman of Citigroup Corporate and Investment Banking, is among at least 32 fundraisers, known as "bundlers" who have raised $300,000 — the maximum allowed by the inaugural committee. Sussman ponied up the maximum, $50,000 in an individual donation. Citigroup, now attempting to survive by downsizing, has already received $25 billion in bailout money, the most of any bank.

In addition, the watchdog group notes, that:

-- Senior executive Mark Gilbert of Lehman Brothers, which got some federal assistance but collapsed before the $700 billion bailout was approved, raised $185,000.

-- Chairman Robert Wolf of UBS Americas raised $100,000.

-- Jennifer Scully, vice president for private wealth management at Goldman Sachs, raised $100,000.

-- Bruce Heyman, managing director of Goldman’s Private Wealth Management Group’s Midwest Region, came up with $50,000.

-- Kobi Brinson, senior vice president and assistant general counsel for Wachovia (recently merged with Wells Fargo), raised $35,000.

Also among the bundlers are executives of hedge funds and private equity funds that have invested in some of the ailing Wall Street giants.

David Arkush, director of Public Citizen's Congress Watch, says "it's no wonder that Wall Street is pouring so much money into this inauguration. The executive branch has given bailouts worth trillions of dollars to Wall Street firms and is considering trillions more. Wall Street has a lot at stake."

Greg Gordon - January 14, 2009 - source McClatchy

Tag this page!

January 18 - 9:19pm.

President-elect Barack Obama has spoken a lot about setting a new standard for ethics and transparency, and he issued an edict that his inaugural committee would bar contributions from corporations, political action committees, lobbyists, labor unions and foreigners.

But as always seems to happen, big financial interests find a way to weigh in with a pile of cash.

The watchdog group Public Citizen says nearly 80 percent of the $35.3 million raised by the Presidential Inaugural Committee to date has come from 211 wealthy donors, including a number from Wall Street firms benefiting from the mushrooming federal bailout.

Louis Sussman, vice chairman of Citigroup Corporate and Investment Banking, is among at least 32 fundraisers, known as "bundlers" who have raised $300,000 — the maximum allowed by the inaugural committee. Sussman ponied up the maximum, $50,000 in an individual donation. Citigroup, now attempting to survive by downsizing, has already received $25 billion in bailout money, the most of any bank.

In addition, the watchdog group notes, that:

-- Senior executive Mark Gilbert of Lehman Brothers, which got some federal assistance but collapsed before the $700 billion bailout was approved, raised $185,000.

-- Chairman Robert Wolf of UBS Americas raised $100,000.

-- Jennifer Scully, vice president for private wealth management at Goldman Sachs, raised $100,000.

-- Bruce Heyman, managing director of Goldman’s Private Wealth Management Group’s Midwest Region, came up with $50,000.

-- Kobi Brinson, senior vice president and assistant general counsel for Wachovia (recently merged with Wells Fargo), raised $35,000.

Also among the bundlers are executives of hedge funds and private equity funds that have invested in some of the ailing Wall Street giants.

David Arkush, director of Public Citizen's Congress Watch, says "it's no wonder that Wall Street is pouring so much money into this inauguration. The executive branch has given bailouts worth trillions of dollars to Wall Street firms and is considering trillions more. Wall Street has a lot at stake."

Greg Gordon - January 14, 2009 - source McClatchy

Tag this page!

Saturday, January 17, 2009

Report: Over 8 in 10 corporations have tax havens

By KEN THOMAS, Associated Press Writer

Fri Jan 16, 6:28 pm ET

WASHINGTON – Eighty-three of the nation's 100 largest corporations, including Citigroup, Bank of America and News Corp., had subsidiaries in offshore tax havens in 2007, and some of the companies received federal bailout funding, a government watchdog said Friday.

The Government Accountability Office released a report that said Bank of America Inc., Citigroup Inc. and Morgan Stanley all had more than 100 units in countries that maintain low or no taxes. The three financial institutions were included in the $700 billion financial bailout approved by Congress.

Insurance giant American International Group Inc., which has received about $150 billion in bailout money, had 18 subsidiaries. JPMorgan Chase & Co. had 50 units and Wells Fargo & Co. had 18; both financial institutions received government bailout money.

Sens. Carl Levin, D-Mich., and Byron Dorgan, D-N.D., who requested the report, have pushed for tougher laws to fight offshore tax havens around the globe. Levin, who leads the Senate Permanent Subcommittee on Investigations, has estimated abusive tax havens and offshore accounts cost the U.S. government at least $100 billion a year in lost taxes.

"I think we should take action to shut down these tax dodgers and we will be introducing legislation to do just that," Dorgan said.

General Motors Corp., which received $13.4 billion from the federal rescue package, had 11 offshore subsidiaries while GM's financing arm, GMAC LLC, had two offshore units. GMAC, whose majority owner is private equity firm Cerberus Capital Management LP, received $5 billion from the Treasury Department in late December.

Citigroup said in a statement that it has more than 4,000 subsidiaries around the globe "which enables us to serve hundreds of millions of individuals and institutions in more than 100 countries." A News Corp. spokeswoman declined comment. Messages were left with several of the companies identified in the report.

Separately, the GAO said 63 of the 100 largest federal contractors maintain subsidiaries in 50 tax havens.

Levin noted that many competitors use the tax havens to varying degrees. PepsiCo Inc. has 70 subsidiaries while the Coca-Cola Co. has eight units. Caterpillar Inc. had 49 while Deere & Co. had three.

"We need to put an end to the use of offshore secrecy jurisdictions as tax havens," Levin said.

The GAO said the subsidiaries could be established in the countries "for a variety of nontax business reasons" and said having a business unit in one of the countries "does not signify that a corporation or federal contractor established that subsidiary for the purpose of reducing its tax burden."

Citigroup had 427 units in 23 countries, including 91 subsidiaries in Luxembourg and 90 in the Cayman Islands. Morgan Stanley had 273 units, News Corp. had 152 and Bank of America had 115. Procter & Gamble Co. had 83 subsidiaries and Pfizer Inc. had 80 in the jurisdictions.

Several major corporations have announced plans to leave Bermuda, a leading offshore business center, amid the global financial crisis and fears of tighter tax rules. Tyco Electronics Ltd., which makes electronic components, and Foster Wheeler Ltd., an engineering and construction company, are reincorporating in Switzerland — which has a tax treaty with the U.S. — for tax and other reasons. Covidien Ltd., a health care products company, is heading to Ireland.

___

On the Net:

U.S. Government Accountability Office: http://www.gao.gov/

Fri Jan 16, 6:28 pm ET

WASHINGTON – Eighty-three of the nation's 100 largest corporations, including Citigroup, Bank of America and News Corp., had subsidiaries in offshore tax havens in 2007, and some of the companies received federal bailout funding, a government watchdog said Friday.

The Government Accountability Office released a report that said Bank of America Inc., Citigroup Inc. and Morgan Stanley all had more than 100 units in countries that maintain low or no taxes. The three financial institutions were included in the $700 billion financial bailout approved by Congress.

Insurance giant American International Group Inc., which has received about $150 billion in bailout money, had 18 subsidiaries. JPMorgan Chase & Co. had 50 units and Wells Fargo & Co. had 18; both financial institutions received government bailout money.

Sens. Carl Levin, D-Mich., and Byron Dorgan, D-N.D., who requested the report, have pushed for tougher laws to fight offshore tax havens around the globe. Levin, who leads the Senate Permanent Subcommittee on Investigations, has estimated abusive tax havens and offshore accounts cost the U.S. government at least $100 billion a year in lost taxes.

"I think we should take action to shut down these tax dodgers and we will be introducing legislation to do just that," Dorgan said.

General Motors Corp., which received $13.4 billion from the federal rescue package, had 11 offshore subsidiaries while GM's financing arm, GMAC LLC, had two offshore units. GMAC, whose majority owner is private equity firm Cerberus Capital Management LP, received $5 billion from the Treasury Department in late December.

Citigroup said in a statement that it has more than 4,000 subsidiaries around the globe "which enables us to serve hundreds of millions of individuals and institutions in more than 100 countries." A News Corp. spokeswoman declined comment. Messages were left with several of the companies identified in the report.

Separately, the GAO said 63 of the 100 largest federal contractors maintain subsidiaries in 50 tax havens.

Levin noted that many competitors use the tax havens to varying degrees. PepsiCo Inc. has 70 subsidiaries while the Coca-Cola Co. has eight units. Caterpillar Inc. had 49 while Deere & Co. had three.

"We need to put an end to the use of offshore secrecy jurisdictions as tax havens," Levin said.

The GAO said the subsidiaries could be established in the countries "for a variety of nontax business reasons" and said having a business unit in one of the countries "does not signify that a corporation or federal contractor established that subsidiary for the purpose of reducing its tax burden."

Citigroup had 427 units in 23 countries, including 91 subsidiaries in Luxembourg and 90 in the Cayman Islands. Morgan Stanley had 273 units, News Corp. had 152 and Bank of America had 115. Procter & Gamble Co. had 83 subsidiaries and Pfizer Inc. had 80 in the jurisdictions.

Several major corporations have announced plans to leave Bermuda, a leading offshore business center, amid the global financial crisis and fears of tighter tax rules. Tyco Electronics Ltd., which makes electronic components, and Foster Wheeler Ltd., an engineering and construction company, are reincorporating in Switzerland — which has a tax treaty with the U.S. — for tax and other reasons. Covidien Ltd., a health care products company, is heading to Ireland.

___

On the Net:

U.S. Government Accountability Office: http://www.gao.gov/

Monday, January 12, 2009

Jews, money and image

Posted on Sun, Jan. 11, 2009

By Stacey Burling

Inquirer Staff Writer

The scholars approached their topic with considerable nervousness, and that was before the Wall Street meltdown, before Bernard L. Madoff.

Would a series of lectures at a premier business school on the history of Jews making money feed negative stereotypes?

In the end, the Wharton School and the Herbert D. Katz Center for Advanced Judaic Studies decided to go ahead and tackle a topic that has gotten short shrift from academics until recently.

The goal, said the center's director, David Ruderman, is to understand Jewish economic history "more profoundly, which is what a university does."

The center and Wharton, which both are part of the University of Pennsylvania, are sponsoring three lectures at Wharton's Huntsman Hall titled "Jews in Business: Between Myth and Reality." The first is Jan. 20.

The presentations grew from a yearlong postdoctoral study program at the Katz Center, which has its own series of speeches on the topic in the community. Each year, 20 fellows from around the world come to the center to study a particular issue. This year, it is Jews, commerce and culture.

"We don't want to be intimidated by the perceptions of Jewish economic life," said Jonathan Karp, a fellow at the Katz Center who teaches Jewish history at Binghamton University and will be the first speaker for the Wharton lectures.

Michael Gibbons, a deputy dean who approved Wharton's role in the lectures, did not respond to repeated requests for comment.

Karp and other visiting scholars at the center said many Jews had indeed done well in modern business and finance. They trace the financial success of Jews in the Western world to a cultural emphasis on education coupled with centuries of persecution that forced Jews to disperse around the world - creating the foundation for global trade networks - and discrimination that shut Jews out of the most prestigious jobs. That honed a talent for spotting opportunity on the fringes of the economic world. Jews were among the first, for example, to see the mass-audience potential in movies and recorded music by black artists, Karp said.

The downside of economic success throughout much of Jewish history was that it fueled resentment and harsh treatment from competing groups, the scholars said.

"If you wanted to criticize Jewish society, you would use their . . . economic success as a stick to beat them with," said Adam Teller, a University of Haifa historian who with Karp and Derek Penslar, of the University of Toronto, proposed devoting this year at the Katz Center to economic history.

Jonathan Sarna, a professor of American Jewish history at Brandeis University who is not involved with the lecture series, said the history of Jews in business was indeed understudied. Historians in general have been less interested in economic than in social history for much of the last century, he said, but Jewish historians have had the extra concern that "their writing would be used against them."

Historians at the center said they had seen little evidence that the current economic crisis or Madoff's audacious alleged fraud have led to an upswing in anti-Semitism. That is a sign that Americans can handle this subject, they said.

"It is a measure of Jews' growing security in America that we feel the topic isn't off-limits," Sarna agreed.

The belief that Jews are good with money cuts both ways, the historians said. There's the dark side of Shakespeare's Shylock and Dickens' Fagin, which bolstered the negative stereotype that Jews were greedy and unsavory. The Protocols of the Elders of Zion, which have been discredited as a forgery, took anti-Semitism to the extreme, contending that Jews conspired to use their wealth to control the world. On the plus side, Jews have been seen as a group whose business acumen could bring communities prosperity.

Whether Jews are disproportionately successful was a matter of contention among the fellows, but they pointed out that there were plenty of examples of Jewish business failures. And there are Jews on all sides of the Wall Street meltdown, from Madoff and his recently alleged $50 billion Ponzi scheme to people who are policing financial abuse and trying to rebuild the economy.

The historians said they had found nothing inherent in Judaism that would lead to financial success or a predisposition to entrepreneurship. In fact, commerce and religion have largely been kept separate in Jewish cultural life, they said.

The one exception is that the Jewish emphasis on education gave Jews an early advantage: literacy and familiarity with numbers.

Jews gravitated toward finance and trade centuries ago, when more highly valued roles in agrarian societies - land owner and warrior - were denied to them. Early Christians were banned from loaning money at interest to fellow Christians, but they needed loans and Jews took on that role.

Over time, the historians said, Jews were seen as trusted middlemen and people who could manage the wealth of powerful landowners. Their lack of a country or land of their own made them less threatening to nobles.

"They empowered themselves with their economic activity," Teller said.

Jews' outsider status also freed them from the more rigid roles of noble, burgher and peasant, which were assigned to European countries' primary populations. They became the "utility infielders" and the business "B-team of premodern society," Karp said. Those roles came with flexibility that helped Jews exploit business opportunities better than some other groups.

Penslar said Jews in the 1500s could never have guessed it, but the competitive, restrictive nature of their lives would leave future generations better positioned for modern capitalism. "The Jews were historically urban and mobile people," he said. They were also entrepreneurial and accustomed to finding opportunity where others had missed it.

"The Jews were excluded for most of the history of Europe from accepted fields of economic activity," Teller said. "They were always looking for different niches."

For more information about the Wharton lectures, contact the Katz Center for Advanced Judaic Studies at 215-238-1290, Ext. 406.

By Stacey Burling

Inquirer Staff Writer

The scholars approached their topic with considerable nervousness, and that was before the Wall Street meltdown, before Bernard L. Madoff.

Would a series of lectures at a premier business school on the history of Jews making money feed negative stereotypes?

In the end, the Wharton School and the Herbert D. Katz Center for Advanced Judaic Studies decided to go ahead and tackle a topic that has gotten short shrift from academics until recently.

The goal, said the center's director, David Ruderman, is to understand Jewish economic history "more profoundly, which is what a university does."

The center and Wharton, which both are part of the University of Pennsylvania, are sponsoring three lectures at Wharton's Huntsman Hall titled "Jews in Business: Between Myth and Reality." The first is Jan. 20.

The presentations grew from a yearlong postdoctoral study program at the Katz Center, which has its own series of speeches on the topic in the community. Each year, 20 fellows from around the world come to the center to study a particular issue. This year, it is Jews, commerce and culture.

"We don't want to be intimidated by the perceptions of Jewish economic life," said Jonathan Karp, a fellow at the Katz Center who teaches Jewish history at Binghamton University and will be the first speaker for the Wharton lectures.

Michael Gibbons, a deputy dean who approved Wharton's role in the lectures, did not respond to repeated requests for comment.

Karp and other visiting scholars at the center said many Jews had indeed done well in modern business and finance. They trace the financial success of Jews in the Western world to a cultural emphasis on education coupled with centuries of persecution that forced Jews to disperse around the world - creating the foundation for global trade networks - and discrimination that shut Jews out of the most prestigious jobs. That honed a talent for spotting opportunity on the fringes of the economic world. Jews were among the first, for example, to see the mass-audience potential in movies and recorded music by black artists, Karp said.

The downside of economic success throughout much of Jewish history was that it fueled resentment and harsh treatment from competing groups, the scholars said.

"If you wanted to criticize Jewish society, you would use their . . . economic success as a stick to beat them with," said Adam Teller, a University of Haifa historian who with Karp and Derek Penslar, of the University of Toronto, proposed devoting this year at the Katz Center to economic history.

Jonathan Sarna, a professor of American Jewish history at Brandeis University who is not involved with the lecture series, said the history of Jews in business was indeed understudied. Historians in general have been less interested in economic than in social history for much of the last century, he said, but Jewish historians have had the extra concern that "their writing would be used against them."

Historians at the center said they had seen little evidence that the current economic crisis or Madoff's audacious alleged fraud have led to an upswing in anti-Semitism. That is a sign that Americans can handle this subject, they said.

"It is a measure of Jews' growing security in America that we feel the topic isn't off-limits," Sarna agreed.

The belief that Jews are good with money cuts both ways, the historians said. There's the dark side of Shakespeare's Shylock and Dickens' Fagin, which bolstered the negative stereotype that Jews were greedy and unsavory. The Protocols of the Elders of Zion, which have been discredited as a forgery, took anti-Semitism to the extreme, contending that Jews conspired to use their wealth to control the world. On the plus side, Jews have been seen as a group whose business acumen could bring communities prosperity.

Whether Jews are disproportionately successful was a matter of contention among the fellows, but they pointed out that there were plenty of examples of Jewish business failures. And there are Jews on all sides of the Wall Street meltdown, from Madoff and his recently alleged $50 billion Ponzi scheme to people who are policing financial abuse and trying to rebuild the economy.

The historians said they had found nothing inherent in Judaism that would lead to financial success or a predisposition to entrepreneurship. In fact, commerce and religion have largely been kept separate in Jewish cultural life, they said.

The one exception is that the Jewish emphasis on education gave Jews an early advantage: literacy and familiarity with numbers.

Jews gravitated toward finance and trade centuries ago, when more highly valued roles in agrarian societies - land owner and warrior - were denied to them. Early Christians were banned from loaning money at interest to fellow Christians, but they needed loans and Jews took on that role.

Over time, the historians said, Jews were seen as trusted middlemen and people who could manage the wealth of powerful landowners. Their lack of a country or land of their own made them less threatening to nobles.

"They empowered themselves with their economic activity," Teller said.

Jews' outsider status also freed them from the more rigid roles of noble, burgher and peasant, which were assigned to European countries' primary populations. They became the "utility infielders" and the business "B-team of premodern society," Karp said. Those roles came with flexibility that helped Jews exploit business opportunities better than some other groups.

Penslar said Jews in the 1500s could never have guessed it, but the competitive, restrictive nature of their lives would leave future generations better positioned for modern capitalism. "The Jews were historically urban and mobile people," he said. They were also entrepreneurial and accustomed to finding opportunity where others had missed it.

"The Jews were excluded for most of the history of Europe from accepted fields of economic activity," Teller said. "They were always looking for different niches."

For more information about the Wharton lectures, contact the Katz Center for Advanced Judaic Studies at 215-238-1290, Ext. 406.

Financial scoundrels have little to fear from the law

If experience is any guide, the titans behind the system's meltdown, and the regulators who watched it take shape, won't pay for their irresponsibility.

"Justice? You get justice in the next world, in this world you have the law."

That opening line of one of my favorite novels, William Gaddis' 1994 legal satire "A Frolic of His Own," comes back to me every time I hear someone call for packing the rich malefactors behind the great financial meltdown of 2008 off to jail.

Having watched 40% of our 401(k)s go up in smoke and jobs vanish by the millions, it's natural to want to see the guilty subjected to divine justice. There's no dearth of suspects.

There are heads of banks and mortgage companies who invested their capital and made loans without the most cursory due diligence -- Angelo Mozilo of Countrywide Financial and Charles Prince of Citigroup come to mind. Richard Fuld and James Cayne, the bosses of Lehman Bros. and Bear Stearns, who presided over the extinction of their fine old firms. Maurice R. “Hank” Greenberg of AIG, whom I saw last year on CNBC saying that a government bailout of that irresponsible company ($150 billion at last count) was in the "national interest."

These execs collected otherworldly salaries and bonuses for years on the grounds that their institutions could scarcely survive a week absent their wisdom and judgment. We know better now, but they haven't given the money back.

Is America's legal system up to the task of delivering the justice they deserve? Experience suggests we're bound to be disappointed. "Before you can punish anybody, you have to determine if there's a crime, and I'm not sure much of this activity is criminal," Clifford Hyatt, a former SEC enforcement lawyer now at Pillsbury Winthrop Shaw Pittman in Los Angeles, told me.

As Gaddis understood, the law (in this world) is preoccupied with discrete misdeeds more than with elemental depravity. Kenneth Lay perpetrated the Enron scheme, but he was indicted for such mundane felonies as lying to employees about the firm's health. Criminal cases involving what's often excused as bad "business judgment" are notoriously difficult and complex, and who wants to see a guilty CEO skate on a technicality?

Let's not forget that much of what passes for justice in the public arena is theater. No one appreciates a good perp walk more than I do (except maybe Nancy Grace). Yet the first frisson of excitement never produces lasting nourishment.

No. 1 on the perp walk hit parade of 1987, for instance, was the arrest of three Wall Street traders allegedly involved in the big insider trading scandal of the moment. As news cameras rolled, one was led tearfully from his trading floor and handcuffed by agents of Rudolph Giuliani, then the federal prosecutor in Manhattan.

The charges against all three were dropped four months later. Who was the net beneficiary of this stunt? Only Giuliani, who gained a political platform that enabled him to infest our national politics for the next 20 years.

And what about those who don't lie or commit outright fraud, but set the stage for disaster? Consider former SEC Chairman Arthur Levitt, who lately has been swanking around lecturing congressmen and the media about the need for rigorous regulation.

Levitt deserves credit for his activism at the SEC on behalf of shareholders. But he led a regulatory hit squad in 1998 that killed an effort to reel in credit default swaps and other derivatives. These fancy unregulated instruments helped bring the international financial system to its knees 10 years later. By the way, Levitt was SEC chief from 1993 to 2001, when Bernard Madoff's alleged fraud was almost certainly already in full cry, and his agency never laid a finger on the man.

How should we punish him for his dereliction of duty? Indict? Stop giving him airtime? Bill him for his SEC salary?

It's hard to find a provision of the penal law that would cover Levitt, former Federal Reserve Chairman Alan Greenspan or former Treasury secretaries Lawrence Summers and Robert Rubin, each of whom played an important role in cooking up the financial meringue that has cost America, and the world, so much. Rubin resigned Friday as an executive of Citigroup, but Summers has been nominated as head of the National Economic Council in the Obama White House.

They all portray the meltdown as something they couldn't have foreseen. "I'm astounded that no one has said, 'I'm sorry,' " said Tamar Frankel, a law professor at Boston University who writes extensively on business morality. She says expressions of shame, guilt and empathy with the victims would go far to restore public confidence in the markets.

But Depression history does give us a template for a public shaming: the so-called Pecora hearings into the 1929 stock market crash. (They were named after the Senate Banking Committee's indefatigable chief counsel, Ferdinand Pecora.)

Pecora had no patience for bankers and financiers such as J.P. Morgan, who swore they'd had only the public's interest at heart when they inflated the stock market bubble. He laid out for the world how America's financial institutions, which had stood for "safety, strength, prudence, and high-mindedness" and were supposedly led by men "possessing almost mythical business genius and foresight" had relied instead on "legal technicians and the complaisance of governmental authorities" to cheat the average investor and foment the Great Crash. (The quotations are from his impassioned 1939 book, "Wall Street Under Oath.")

Pecora's chief target was Charles E. Mitchell, chairman of the National City Bank -- precursor of Citigroup, one of the least prudent banks in the current mess. Mitchell was never criminally indicted for his role in the crash, but Pecora made sure his reputation for probity was exposed as a complete sham. National City fired him shortly after the hearings.

An inquisition such as Pecora's is the minimum we should have, short of indictment and trial.

It will be said that many big financial perps are getting their comeuppance today via the destruction of their personal fortunes, as though being pared back to a seven-digit net from nine digits is tougher on them than three to five in San Quentin would be to a kid from the projects.

Does anyone buy that? The notion brings to mind a quote from Willa Cather's 1922 novel "One of Ours": "Even the wicked get worse than they deserve," she wrote. But Cather lived in more indulgent times.

Michael Hiltzik's column runs every Monday and Thursday. You can reach him at michael.hiltzik@latimes.com, and read his archived columns at latimes.com/hiltzik.

That opening line of one of my favorite novels, William Gaddis' 1994 legal satire "A Frolic of His Own," comes back to me every time I hear someone call for packing the rich malefactors behind the great financial meltdown of 2008 off to jail.

Having watched 40% of our 401(k)s go up in smoke and jobs vanish by the millions, it's natural to want to see the guilty subjected to divine justice. There's no dearth of suspects.

There are heads of banks and mortgage companies who invested their capital and made loans without the most cursory due diligence -- Angelo Mozilo of Countrywide Financial and Charles Prince of Citigroup come to mind. Richard Fuld and James Cayne, the bosses of Lehman Bros. and Bear Stearns, who presided over the extinction of their fine old firms. Maurice R. “Hank” Greenberg of AIG, whom I saw last year on CNBC saying that a government bailout of that irresponsible company ($150 billion at last count) was in the "national interest."

These execs collected otherworldly salaries and bonuses for years on the grounds that their institutions could scarcely survive a week absent their wisdom and judgment. We know better now, but they haven't given the money back.

Is America's legal system up to the task of delivering the justice they deserve? Experience suggests we're bound to be disappointed. "Before you can punish anybody, you have to determine if there's a crime, and I'm not sure much of this activity is criminal," Clifford Hyatt, a former SEC enforcement lawyer now at Pillsbury Winthrop Shaw Pittman in Los Angeles, told me.

As Gaddis understood, the law (in this world) is preoccupied with discrete misdeeds more than with elemental depravity. Kenneth Lay perpetrated the Enron scheme, but he was indicted for such mundane felonies as lying to employees about the firm's health. Criminal cases involving what's often excused as bad "business judgment" are notoriously difficult and complex, and who wants to see a guilty CEO skate on a technicality?

Let's not forget that much of what passes for justice in the public arena is theater. No one appreciates a good perp walk more than I do (except maybe Nancy Grace). Yet the first frisson of excitement never produces lasting nourishment.

No. 1 on the perp walk hit parade of 1987, for instance, was the arrest of three Wall Street traders allegedly involved in the big insider trading scandal of the moment. As news cameras rolled, one was led tearfully from his trading floor and handcuffed by agents of Rudolph Giuliani, then the federal prosecutor in Manhattan.

The charges against all three were dropped four months later. Who was the net beneficiary of this stunt? Only Giuliani, who gained a political platform that enabled him to infest our national politics for the next 20 years.

And what about those who don't lie or commit outright fraud, but set the stage for disaster? Consider former SEC Chairman Arthur Levitt, who lately has been swanking around lecturing congressmen and the media about the need for rigorous regulation.

Levitt deserves credit for his activism at the SEC on behalf of shareholders. But he led a regulatory hit squad in 1998 that killed an effort to reel in credit default swaps and other derivatives. These fancy unregulated instruments helped bring the international financial system to its knees 10 years later. By the way, Levitt was SEC chief from 1993 to 2001, when Bernard Madoff's alleged fraud was almost certainly already in full cry, and his agency never laid a finger on the man.

How should we punish him for his dereliction of duty? Indict? Stop giving him airtime? Bill him for his SEC salary?

It's hard to find a provision of the penal law that would cover Levitt, former Federal Reserve Chairman Alan Greenspan or former Treasury secretaries Lawrence Summers and Robert Rubin, each of whom played an important role in cooking up the financial meringue that has cost America, and the world, so much. Rubin resigned Friday as an executive of Citigroup, but Summers has been nominated as head of the National Economic Council in the Obama White House.

They all portray the meltdown as something they couldn't have foreseen. "I'm astounded that no one has said, 'I'm sorry,' " said Tamar Frankel, a law professor at Boston University who writes extensively on business morality. She says expressions of shame, guilt and empathy with the victims would go far to restore public confidence in the markets.

But Depression history does give us a template for a public shaming: the so-called Pecora hearings into the 1929 stock market crash. (They were named after the Senate Banking Committee's indefatigable chief counsel, Ferdinand Pecora.)

Pecora had no patience for bankers and financiers such as J.P. Morgan, who swore they'd had only the public's interest at heart when they inflated the stock market bubble. He laid out for the world how America's financial institutions, which had stood for "safety, strength, prudence, and high-mindedness" and were supposedly led by men "possessing almost mythical business genius and foresight" had relied instead on "legal technicians and the complaisance of governmental authorities" to cheat the average investor and foment the Great Crash. (The quotations are from his impassioned 1939 book, "Wall Street Under Oath.")

Pecora's chief target was Charles E. Mitchell, chairman of the National City Bank -- precursor of Citigroup, one of the least prudent banks in the current mess. Mitchell was never criminally indicted for his role in the crash, but Pecora made sure his reputation for probity was exposed as a complete sham. National City fired him shortly after the hearings.

An inquisition such as Pecora's is the minimum we should have, short of indictment and trial.

It will be said that many big financial perps are getting their comeuppance today via the destruction of their personal fortunes, as though being pared back to a seven-digit net from nine digits is tougher on them than three to five in San Quentin would be to a kid from the projects.

Does anyone buy that? The notion brings to mind a quote from Willa Cather's 1922 novel "One of Ours": "Even the wicked get worse than they deserve," she wrote. But Cather lived in more indulgent times.

Michael Hiltzik's column runs every Monday and Thursday. You can reach him at michael.hiltzik@latimes.com, and read his archived columns at latimes.com/hiltzik.

Wednesday, January 7, 2009

New papers filed in Madoff case

By LARRY NEUMEISTER, Associated Press Writer Larry Neumeister,

wednesday,07,20092 hrs 19 mins ago

NEW YORK – Disgraced financier Bernard Madoff and his wife sent at least 16 watches, a jade necklace and a diamond bracelet to family and relatives, proving he will continue to dissipate what little is left from his $50 billion fraud, a prosecutor told a judge in arguing that Madoff be jailed.

Assistant U.S. Attorney Marc Litt said in a letter released Wednesday that Madoff violated a court order barring him from dissipating, concealing or disposing of any assets when he and his wife sent the items to close relatives and two friends.

"The need for detention in this case is clear," Litt wrote in a letter to Magistrate Judge Ronald L. Ellis. "The continued release of the defendant presents a danger to the community of additional harm and further obstruction of justice."

Madoff was arrested Dec. 11 on a securities fraud charge after the FBI said he confessed to swindling investors. Authorities say he told his sons he ran a $50 billion Ponzi scheme and had only a few hundred million dollars left.

Although he has been freed on $10 million bail, he has been confined to his $7 million Manhattan penthouse with an electronic bracelet and 24-hour guard.

During a bail hearing Monday, Ellis asked Litt and defense lawyer Ira Sorkin to file documents explaining their positions after Litt said Madoff should lose his freedom. Sorkin's filing was due later Wednesday.

"Our comments will be contained in our filing with the court," Sorkin said.

A criminal complaint against Madoff said the former Nasdaq chairman had offered to distribute between $200 million and $300 million that remained in his company's accounts to close relatives and friends before he surrendered to authorities.

The bail battle continued as Securities Investor Protection Corp. President Stephen Harbeck said through a spokeswoman that investors who lost money with Madoff could begin recovering some of their funds within two months if their accounts are easy to trace.

In his six-page letter sent to Ellis Tuesday night and publicly filed Wednesday, Litt said Madoff violated his promise not to touch his assets when he and his wife sent multiple package on Dec. 24 to relatives and friends.

The prosecutor said one package contained 13 watches, one diamond necklace, an emerald ring, and two sets of cufflinks, items estimated to be worth more than $1 million.

He said two other packages contained a diamond bracelet, a gold watch, a diamond Cartier watch, a diamond Tiffany watch, four diamond brooches, a jade necklace and other assorted jewelry and were sent to relatives.

Litt said the contents of those packages have been recovered, but prosecutors have not yet learned the contents of two additional packages sent to Madoff's brother and an unidentified couple in Florida.

The prosecutor wrote that there was also a serious risk that Madoff would flee because he has "admitted to having perpetrated one of the largest frauds in history — a giant Ponzi scheme that likely involves losses in the tens of billions of dollars."

At Monday's bail hearing, Sorkin argued that Madoff's wife sent the expensive jewelry when she was not under a court order barring her from doing so, and Madoff did not do anything that showed him to be a threat to the community.

"If he was found to be selling narcotics, if it's found that he threatened somebody, if it's found that he was fleeing the community, then I think your honor should consider new bail conditions," Sorkin told the judge Monday. "But that's not the case here."

Attorney Jerry Reisman, representing 13 Madoff investors, said he believes Madoff should be sent to jail. He said his clients are "astounded" and "infuriated" that Madoff remains out on bail and suspect he still will try to hide assets.

In other developments related to the Madoff scandal:

_A former executive of the Securities and Exchange Commission's New York branch told the New York Post she was upset that she was singled out by a Madoff whistleblower as someone who should have detected the alleged fraud. "Why are you taking a midlevel staff person and making me responsible for the failure of the American economy?" Meaghan Cheung said.

_New York University received continuation of a restraining order against the fund run by GMAC Chairman Ezra Merkin, through which the university says it has lost as much as $94 million, the Post reported.

wednesday,07,20092 hrs 19 mins ago

NEW YORK – Disgraced financier Bernard Madoff and his wife sent at least 16 watches, a jade necklace and a diamond bracelet to family and relatives, proving he will continue to dissipate what little is left from his $50 billion fraud, a prosecutor told a judge in arguing that Madoff be jailed.

Assistant U.S. Attorney Marc Litt said in a letter released Wednesday that Madoff violated a court order barring him from dissipating, concealing or disposing of any assets when he and his wife sent the items to close relatives and two friends.

"The need for detention in this case is clear," Litt wrote in a letter to Magistrate Judge Ronald L. Ellis. "The continued release of the defendant presents a danger to the community of additional harm and further obstruction of justice."

Madoff was arrested Dec. 11 on a securities fraud charge after the FBI said he confessed to swindling investors. Authorities say he told his sons he ran a $50 billion Ponzi scheme and had only a few hundred million dollars left.

Although he has been freed on $10 million bail, he has been confined to his $7 million Manhattan penthouse with an electronic bracelet and 24-hour guard.

During a bail hearing Monday, Ellis asked Litt and defense lawyer Ira Sorkin to file documents explaining their positions after Litt said Madoff should lose his freedom. Sorkin's filing was due later Wednesday.

"Our comments will be contained in our filing with the court," Sorkin said.

A criminal complaint against Madoff said the former Nasdaq chairman had offered to distribute between $200 million and $300 million that remained in his company's accounts to close relatives and friends before he surrendered to authorities.

The bail battle continued as Securities Investor Protection Corp. President Stephen Harbeck said through a spokeswoman that investors who lost money with Madoff could begin recovering some of their funds within two months if their accounts are easy to trace.

In his six-page letter sent to Ellis Tuesday night and publicly filed Wednesday, Litt said Madoff violated his promise not to touch his assets when he and his wife sent multiple package on Dec. 24 to relatives and friends.

The prosecutor said one package contained 13 watches, one diamond necklace, an emerald ring, and two sets of cufflinks, items estimated to be worth more than $1 million.

He said two other packages contained a diamond bracelet, a gold watch, a diamond Cartier watch, a diamond Tiffany watch, four diamond brooches, a jade necklace and other assorted jewelry and were sent to relatives.

Litt said the contents of those packages have been recovered, but prosecutors have not yet learned the contents of two additional packages sent to Madoff's brother and an unidentified couple in Florida.

The prosecutor wrote that there was also a serious risk that Madoff would flee because he has "admitted to having perpetrated one of the largest frauds in history — a giant Ponzi scheme that likely involves losses in the tens of billions of dollars."

At Monday's bail hearing, Sorkin argued that Madoff's wife sent the expensive jewelry when she was not under a court order barring her from doing so, and Madoff did not do anything that showed him to be a threat to the community.

"If he was found to be selling narcotics, if it's found that he threatened somebody, if it's found that he was fleeing the community, then I think your honor should consider new bail conditions," Sorkin told the judge Monday. "But that's not the case here."

Attorney Jerry Reisman, representing 13 Madoff investors, said he believes Madoff should be sent to jail. He said his clients are "astounded" and "infuriated" that Madoff remains out on bail and suspect he still will try to hide assets.

In other developments related to the Madoff scandal:

_A former executive of the Securities and Exchange Commission's New York branch told the New York Post she was upset that she was singled out by a Madoff whistleblower as someone who should have detected the alleged fraud. "Why are you taking a midlevel staff person and making me responsible for the failure of the American economy?" Meaghan Cheung said.

_New York University received continuation of a restraining order against the fund run by GMAC Chairman Ezra Merkin, through which the university says it has lost as much as $94 million, the Post reported.

Tuesday, January 6, 2009

German mogul kills self over financial meltdown

By GEIR MOULSON,

Associated Press Writer Geir Moulson, Associated Press Writer,Tuesday 05,2009 1 hr 50 mins ago

BERLIN – German billionaire Adolf Merckle has committed suicide after his business empire, which included interests ranging from pharmaceuticals to cement, ran into trouble in the global financial crisis, his family said Tuesday.

The 74-year-old's body was found Monday night on railway tracks at Blaubeuren in southwestern Germany, prosecutors in nearby Ulm said in a statement. They described the death as a "railway accident" and said there was no evidence that anyone else was to blame.

His family, which had reported Merckle missing after he failed to return home Monday, issued a brief statement saying he took his own life. A person close to the investigation, who requested anonymity because he was not authorized to speak with the media, said Merckle left a suicide note. Its contents were not divulged.

Merckle's holding company, VEM Vermoegensverwaltung, recently had been in talks with banks to secure credit after its business interests ran up high levels of debt, and also lost value amid the global financial crisis.

The company declined to say how much it needed, or to comment on German media reports that it might have to sell some of its interests.

In addition, the holding company recently said it had suffered heavy losses on shares of automaker Volkswagen AG, which fluctuated wildly last fall as fellow car maker Porsche SE moved to increase its stake in the company.

"Adolf Merckle lived and worked for his family and his firms," the family statement said.

"The distress to his firms caused by the financial crisis and the related uncertainties of recent weeks, along with the helplessness of no longer being able to act, broke the passionate family businessman, and he ended his life," it said.

Merckle's business interests included generic drug maker Ratiopharm International GmbH and cement maker HeidelbergCement AG.

Merckle helped turn his grandfather's chemical wholesale company into one of Germany's biggest pharmaceutical wholesalers, Phoenix Pharmahandel, in which he held a 57 percent stake.

He used his wealth, estimated by Forbes last year to be $9.2 billion, to take stakes in HeidelbergCement and Ratiopharm. HeidelbergCement shares were down 5.8 percent at euro31.39 ($43.18) in Frankfurt trading after news broke of Merckle's death.

Merckle also owned stakes in companies that made a wide array of goods from all-terrain vehicles, software to textiles.

The governor of Merckle's home state of Baden-Wuerttemberg, Guenther Oettinger, said the region had lost a "great entrepreneurial personality" who built up a "business of European significance."

Merckle was awarded Germany's highest decoration, the Bundesverdienstkreuz, in 2005.

Despite his wealth and prominence in corporate Germany, Merckle mostly avoided publicity. He is survived by his wife, Ruth, and four children.

____

Associated Press Writer Oliver Schmale contributed to this report from Stuttgart, Germany.

Associated Press Writer Geir Moulson, Associated Press Writer,Tuesday 05,2009 1 hr 50 mins ago

BERLIN – German billionaire Adolf Merckle has committed suicide after his business empire, which included interests ranging from pharmaceuticals to cement, ran into trouble in the global financial crisis, his family said Tuesday.

The 74-year-old's body was found Monday night on railway tracks at Blaubeuren in southwestern Germany, prosecutors in nearby Ulm said in a statement. They described the death as a "railway accident" and said there was no evidence that anyone else was to blame.

His family, which had reported Merckle missing after he failed to return home Monday, issued a brief statement saying he took his own life. A person close to the investigation, who requested anonymity because he was not authorized to speak with the media, said Merckle left a suicide note. Its contents were not divulged.

Merckle's holding company, VEM Vermoegensverwaltung, recently had been in talks with banks to secure credit after its business interests ran up high levels of debt, and also lost value amid the global financial crisis.

The company declined to say how much it needed, or to comment on German media reports that it might have to sell some of its interests.

In addition, the holding company recently said it had suffered heavy losses on shares of automaker Volkswagen AG, which fluctuated wildly last fall as fellow car maker Porsche SE moved to increase its stake in the company.

"Adolf Merckle lived and worked for his family and his firms," the family statement said.

"The distress to his firms caused by the financial crisis and the related uncertainties of recent weeks, along with the helplessness of no longer being able to act, broke the passionate family businessman, and he ended his life," it said.

Merckle's business interests included generic drug maker Ratiopharm International GmbH and cement maker HeidelbergCement AG.

Merckle helped turn his grandfather's chemical wholesale company into one of Germany's biggest pharmaceutical wholesalers, Phoenix Pharmahandel, in which he held a 57 percent stake.

He used his wealth, estimated by Forbes last year to be $9.2 billion, to take stakes in HeidelbergCement and Ratiopharm. HeidelbergCement shares were down 5.8 percent at euro31.39 ($43.18) in Frankfurt trading after news broke of Merckle's death.

Merckle also owned stakes in companies that made a wide array of goods from all-terrain vehicles, software to textiles.

The governor of Merckle's home state of Baden-Wuerttemberg, Guenther Oettinger, said the region had lost a "great entrepreneurial personality" who built up a "business of European significance."

Merckle was awarded Germany's highest decoration, the Bundesverdienstkreuz, in 2005.

Despite his wealth and prominence in corporate Germany, Merckle mostly avoided publicity. He is survived by his wife, Ruth, and four children.

____

Associated Press Writer Oliver Schmale contributed to this report from Stuttgart, Germany.

Sunday, January 4, 2009

The Wall Street Ponzi Scheme called Fractional Reserve Banking

The Wall Street Ponzi Scheme called Fractional Reserve Banking

mintdollar.com

Borrowing from Peter to Pay Paul

Cartoon in the New Yorker: A gun-toting man with large dark glasses, large hat pulled down, stands in front of a bank teller, who is reading a demand note. It says, “Give me all the money in my account.”Bernie Madoff showed us how it was done: you induce many investors to invest their money, promising steady above-market returns; and you deliver – at least on paper. When your clients check their accounts, they see that their investments have indeed increased by the promised amount. Anyone who opts to pull out of the game is paid promptly and in full. You can afford to pay because most players stay in, and new players are constantly coming in to replace those who drop out. The players who drop out are simply paid with the money coming in from new recruits. The scheme works until the market turns and many players want their money back at once. Then it’s game over: you have to admit that you don’t have the funds, and you are probably looking at jail time.

A Ponzi scheme is a form of pyramid scheme in which earlier investors are paid with the money of later investors rather than from real profits. The perpetuation of the scheme requires an ever-increasing flow of money from investors in order to keep it going. Charles Ponzi was an engaging Boston ex-convict who defrauded investors out of $6 million in the 1920s by promising them a 400 percent return on redeemed postal reply coupons. When he finally could not pay, the scam earned him ten years in jail; and Bernie Madoff is likely to wind up there as well.

Most people are not involved in illegal Ponzi schemes, but we do keep our money in accounts that are tallied on computer screens rather than in stacks of coins or paper bills. How do we know that when we demand our money from our bank or broker that the funds will be there? The fact that banks are subject to “runs” (recall Northern Rock, Indymac and Washington Mutual) suggests that all may not be as it seems on our online screens. Banks themselves are involved in a sort of Ponzi scheme, one that has been perpetuated for hundreds of years. What distinguishes the legal scheme known as “fractional reserve” lending from the illegal schemes of Bernie Madoff and his ilk is that the bankers’ scheme is protected by government charter and backstopped with government funds. At last count, the Federal Reserve and the U.S. Treasury had committed $8.5 trillion to bailing out the banks from their follies.1 By comparison, M2, the largest measure of the money supply now reported by the Federal Reserve, was just under $8 trillion in December 2008.2 The sheer size of the bailout efforts indicates that the banking scheme has reached its mathematical limits and needs to be superseded by something more sustainable.Penetrating the Bankers’ Ponzi Scheme

What fractional reserve lending is and how it works is summed up in Wikipedia as follows:

“Fractional-reserve banking is the banking practice in which banks keep only a fraction of their deposits in reserve (as cash and other liquid assets) with the choice of lending out the remainder, while maintaining the simultaneous obligation to redeem all deposits immediately upon demand. This practice is universal in modern banking. . . .The nature of fractional-reserve banking is that there is only a fraction of cash reserves available at the bank needed to repay all of the demand deposits and banknotes issued. . . . When Fractional-reserve banking works, it works because:

“1. Over any typical period of time, redemption demands are largely or wholly offset by new deposits or issues of notes. The bank thus needs only to satisfy the excess amount of redemptions.“2. Only a minority of people will actually choose to withdraw their demand deposits or present their notes for payment at any given time.“3. People usually keep their funds in the bank for a prolonged period of time.“4. There are usually enough cash reserves in the bank to handle net redemptions.

“If the net redemption demands are unusually large, the bank will run low on reserves and will be forced to raise new funds from additional borrowings (e.g. by borrowing from the money market or using lines of credit held with other banks), and/or sell assets, to avoid running out of reserves and defaulting on its obligations. If creditors are afraid that the bank is running out of cash, they have an incentive to redeem their deposits as soon as possible, triggering a bank run.”

Like in other Ponzi schemes, bank runs result because the bank does not actually have the funds necessary to meet all its obligations. Peter’s money has been lent to Paul, with the interest income going to the bank.

As Elgin Groseclose, Director of the Institute for International Monetary Research, wryly observed in 1934: